The Most Important Thing, Part II (2026)

Is to Know What You Own, and Why You Own It

“Reality is not always probable, or likely.”

-Jorge Luis Borges

The Doom of Continued War Is Recession

The United States has been at war with Iran for 25 days. The magnitude of their folly is now finally occurring to the current administration as evidenced by their repeated and increasingly frantic overtures of peace. But the enemy gets a vote over when hostilities are complete, and the Iranian regime seems reluctant to surrender their pricing power and new monopoly on oil exports transiting the Strait of Hormuz. The only path to victory for the United States is to embargo all oil shipments from Iran, a move which would force oil prices higher and thus spell electoral doom for the party in power.

Seldom does life produce such scenarios with only bad choices. While we would place our bets on the President’s cowardice, and accordingly the likelihood of his ‘bugging out and going home’, ultimately this regime is conducted according to the principle of Willkürherrschaft, rule by caprice—which is to say no principle at all, save for the whim of a 79-year-old failed real estate developer and B-list celebrity of no impulse control who has spent his life running away from catastrophes he himself has engendered but has no ability to resolve. We cannot know with any precision his state of mind at any given time, and so do not place bets.

The conflict seems to have arrived at escalation equilibrium, wherein the actors, having peered over the cliff, decide to take a step back rather than leaping from it, but perhaps still kick a few loose stones over the precipice as if to test gravity. While the United States and the rest of the world have strong incentives to pause here, the US’ allies, Israel and Saudi, operate from a different set of incentives that encourage them to prolong the engagement. Both gain from Iran’s diminution as a regional power, but whereas the House of Saud stands to gain from higher oil prices, Israel’s political right gains from a forever war. The President’s political and personal fortunes rely on the satisfaction of both of these parties, rendering it impossible to choose the interests of the country over his own. When we say that the Presidency is a sacred trust, and this president has broken it, this is what we mean.

Boots on the ground are the next escalatory move for the president, a quite unusual step to take in a war that is already won and basically over. The goal of such a deployment would likely be to capture Kharg Island, Iran’s oil terminal, and perhaps occupy the Strait itself. But Iranian regular and irregular forces would still possess the ability to strike transiting ships from land and thus shut off the flow of 25% of global energy supplies completely. Iran’s proxies in Yemen, the Houthis, can also threaten ships transiting the Bab el-Mandeb Strait just as they did in 2024, taking 4 million barrels of oil per day off the market. It is not hard to imagine a terrorist-type action against any ship transiting the Suez Canal that resulted in a full blockage of the waterway, as happened inadvertently in 2021. That would result in another 5 million barrels per day lost. Easily 30% of world oil supply could be lost due to further escalation—and this is just energy, not to mention gas and a host of other intermediate goods that flow through this part of the world.

We consider these matters at what was previously the peak valuation of US—which is to say, global—equities. These valuations were determined based on implied earnings growth rates or expected multiple expansions that could be said to be lofty if they weren’t quite so ethereal. Prices have yet to be reevaluated in light of the falling sales figures and margin compression that occur as a result of war. Prior to this engagement, US productivity growth had fallen dramatically while inflation was mounting, facts concomitant with the late stages of economic expansions. The only supplement to growth has been the extraordinary capital expenditure committed by the largest tech companies in the world—yet another activity that companies undertake at the end of expansions.

Wars are inflationary, and wars at the nexus of critical global resources especially so. Global Central Banks are watching developments in Iran with great interest but not waiting to let the world know that they are not eager to relax interest rates. Market rates of interest have accordingly risen, providing the financial tightening that they may no longer have to undertake on their own. But the increase in the price of money will be felt acutely in the worlds of Private Equity and Private Credit, not to mention the marginal credits that avail themselves of the high yield markets from time to time. Signs of distress have already begun to appear in the Private Credit space, but with 50 basis points of easing burnt off from the horizon like fog beneath the mid-morning sun will now grow the more common.

As Central Bankers are fond of saying, business cycles do not die of old age; they are murdered. What they are not fond of saying is that they are often murdered by higher interest rates (often wielded by Central Bankers.) A de facto rise in interest rates, along with higher energy prices, should now provide the backdrop necessary for credit and equity to rerate lower in anticipation of lower growth, higher inflation, and higher interest rates. The price of cash has gone up, and what levered companies need is cash. The withdrawal of liquidity from the markets will have reverberating effects that investors are unprepared for, and institutional investors who cannot sell their private investments will, like in 2008, sell what they can: public investments. This would undermine the source of wealth that has kept spending going over the last few years, the equity market, and result in a drawdown in consumer economy—and with it, the rest of the economy.

Thus, a continued war would be very costly not only in the only currency that really matters—human life—but also to the US and global economy. Let us hope that a resolution, real or pretended, is near.

What to Own and Why to Own It

Every so often, we take a step back and describe our current portfolio so that our investors and readers can understand how we think about investing. As we wrote at the beginning of the year, the most important thing is knowing what’s priced in; but the other most important thing is knowing what you own, and why you own it. This ensures that you are able to take advantage of what is or isn’t priced in. This is not investment advice, and you shouldn’t trade on what you read here today. If what you read is of interest, please feel free to reach out directly about how we can help you or your organization prepare for the road ahead.

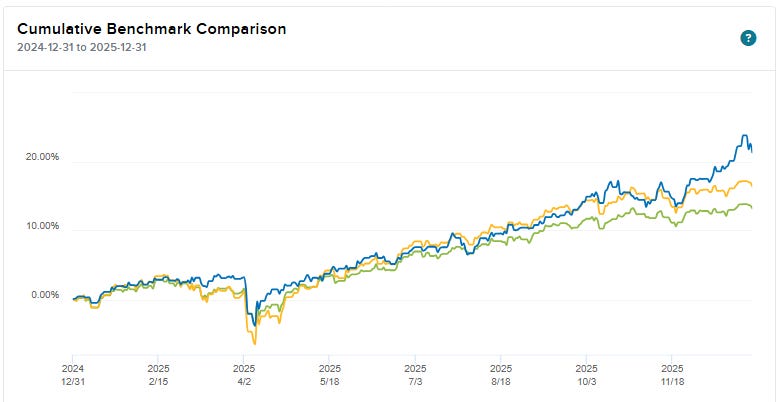

First, we began 2026 on solid footing as our views were validated by the market. Our standard, unlevered portfolio of liquid investments posted an impressive performance. Below compares the performance of this strategy with both a 60%/40% portfolio of equities and bonds (yellow), as well as a 40%/60% portfolio of the same (green).

21.38% return at 1x leverage

9.37% annualized volatility

Sharpe Ratio: 1.65

Best day: 3.67%; Worst day: -3.7%

Max Drawdown: 7.22%

Compared to the S&P 500, to which we do not benchmark our portfolios, but with which most people are familiar, our portfolios performed far better on both an outright and a risk-adjusted basis:

17.29% return

19.05% annualized volatility

Sharpe Ratio: 0.71

Max Drawdown: 18.76%

Again, we don’t benchmark to the SPX, but to use it as a point of comparison, our correlation was 0.70, our beta was 0.34, and our information ration was 4.60. Our portfolio was more than twice as efficient at generating return per unit of risk as the S&P, generating more return with less than half of the risk as measured by volatility, and nearly a third of the risk as measured by downside risk.

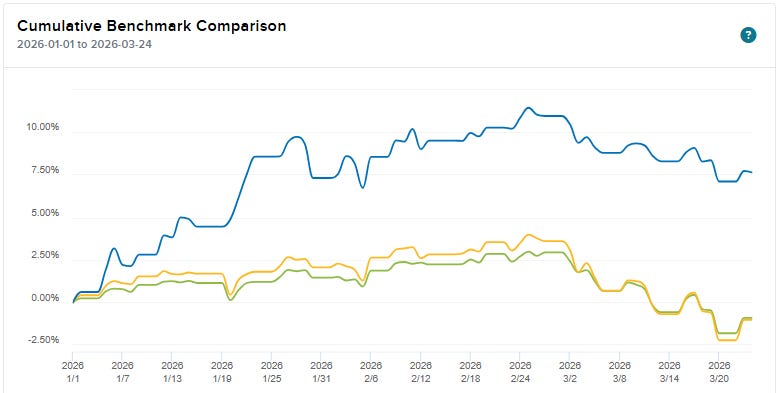

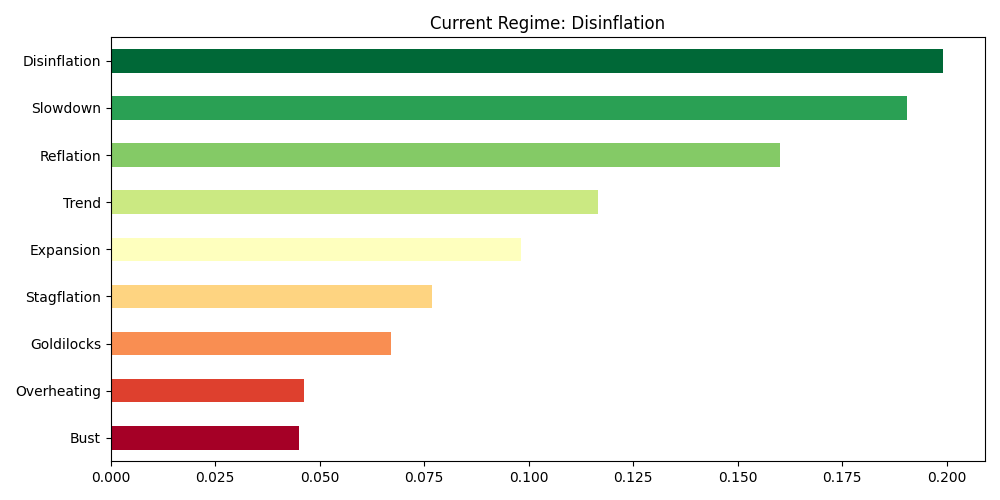

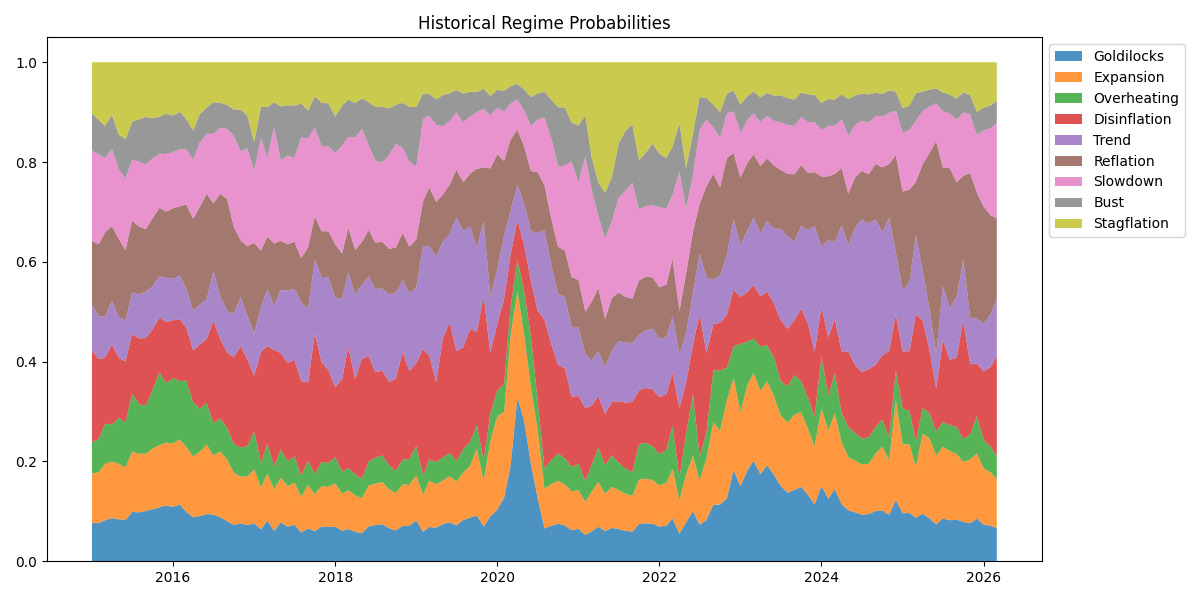

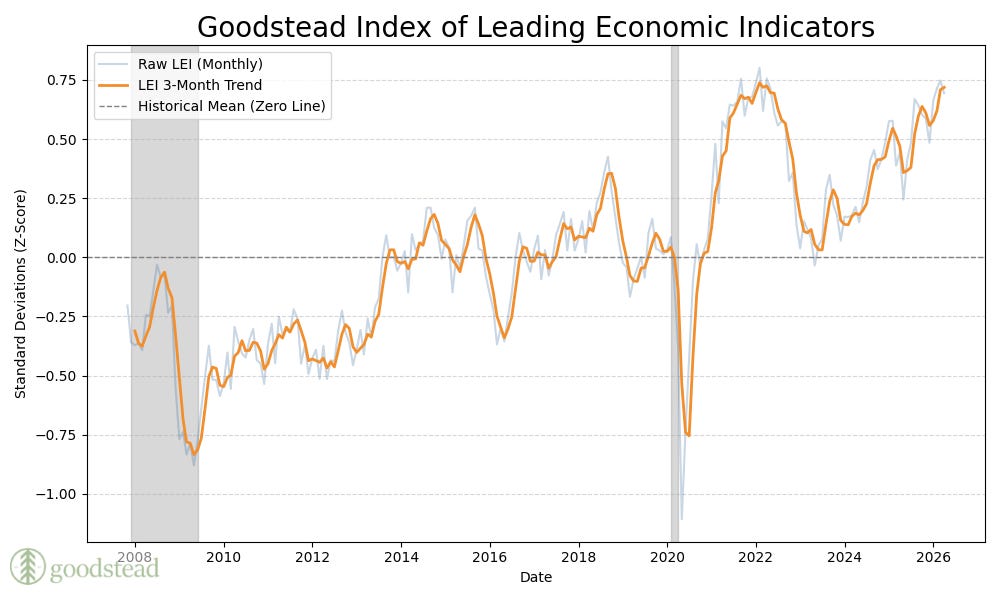

In January and February, while most managers posted losses, we continued to produce gains. As we mentioned last week, we shifted our portfolio from an investment set consistent with late expansion to one that performs well during slowdowns. The macroeconomic indicators we use to inform our investment process counseled such a move. That shift meant that we were well positioned to endure a period of rising inflation, slowing growth, and rising volatility—which is about what we would expect as fallout from a war. While we are in drawdown at the moment—as are all risk assets—we have held onto gains for the year.

Obviously, the world can change at any moment, and the markets can gap down 20% from here. In fact, that is what we expect them to do, which is why we are in the portfolio we are. Without getting into the details of our specific allocations or investment choices—these differ for all of our clients depending upon their risk aversion, ability to bear risk, and investment horizon—the following is an approximation of a portfolio for an average investor with a typical level of risk aversion and an investment horizon of one business cycle or longer. Positions are listed in order of largest to smallest.

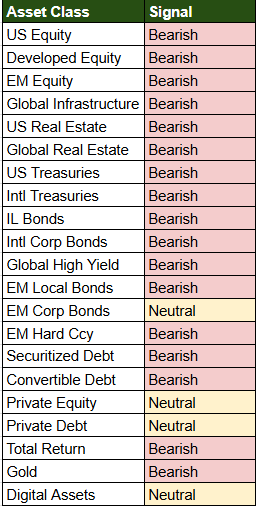

Cash: Leading up to the Iran War, the equity risk premium, or the amount of return you get paid for holding equities over holding bonds, was negative. This is a good signal that risk aversion is too low to produce accurate pricing in markets. Equities, especially growth equities, are overvalued. Credit spreads are too tight, reflecting complacence by credit investors or a belief that corporations will have all the money they need to service their debt. These are just ways of saying stocks and bonds are too expensive relative to the cash flows they will throw off. In environments like this, it pays to go on a buyer’s strike and hold liquidity for when eventually the market will beg for it.

Volatility: When equity and fixed income markets sell off, cash does not gain in price. While it blunts the impact of falling prices on the portfolio, it does nothing by itself to provide positive performance. Long volatility investments, however, provide positive convexity in such environments, counteracting with their rapid price appreciation the rapid price deterioration of short volatility assets. Included among our long volatility bets are our investments in Commodity Trading Advisors, Global Macro Managers, and other managers that employ alternatives.

It is important to remember: Carry is the return to certainty; Volatility is the return to uncertainty. Carry is what you get when you get what you expected, while Volatility is what you get when you get what you least expected.

Short-Duration Inflation Linked Bonds: A real asset, their principal and coupon payments are indexed to the Consumer Price Index. Often their sensitivity to interest rates dominates their sensitivity to inflation rates, making them imperfect inflation hedges over the short term. However, over the longer term they are fit vehicles for transferring wealth into the future, and even better when bought when inflation expectations are lower than realized inflation.

USD-denominated Emerging Market Bonds: Emerging Market Bonds feature a credit premium to developed world sovereign bonds. These credits have been improving relative to their developed world counterparts, either because of fiscal discipline learned from hard lessons about borrowing on the international credit markets in the runup to the Global Financial Crisis, or their economic base as commodity producers or low value-added manufacturers. (These lattermost face headwinds in a world of more expensive energy.) While we would ordinarily take the Emerging Market currency exposure that can be packaged into emerging market debt, we comment on that position later.

Green/Cleaner Energy: We own positions in clean energy and less carbon-intensive energy for two reasons: these became cheap relative to their installed capital base as a result of stated energy policy biases of the current administration, and we love buying things on sale, and; carbon-based energy is in secular decline, and we want to invest in growth, as well as energy sources that promise a future for our children and our children’s children. Further, as oil becomes more expensive, its substitutes become relatively less so. In the soil of oil’s demand destruction are buried the seeds of green energy’s supply growth. This category includes our investments in transition metals and rare earths.

European Equities: These are getting hit at present because of higher energy prices and higher expected interest rates but provide an opportunity to get exposure to equity risk premium at a more reasonable price. Further, administration economic policies make it more likely that the Europe trades more with itself and the rest of the world and with less friction lost to tariffs and trade policy uncertainty. Here we have done well in past with defense and finance companies, and we expect these to continue to perform.

Low Volatility Global Equities: When US growth falls, and global growth along with it, all equities suffer, even those defensive equities that investors think are safe from a fall in price. Low volatility stocks fall in price less and offer free cash flow that makes up for losses in price. Demand for liquidity makes these cash flows worth more as the market cycle turns.

Agricultural Commodities/Farmland: Commodities are excellent hedges against inflation. Because their production is carbon-intensive (fertilizers, machinery), and people can’t get by without them, their price action is correlated with energy commodities. Ag is essentially oil transformed into edible form. A global good, it is reasonably sensitive to global growth. The vagaries of climate change make its supply less and less dependable, providing an opportunity for climate-risk harnessing return.

Global Real Estate Investment Trusts: Another example of Real Assets, over the long run REITS provide cash flows that are indexed to inflation. Near term, as they are publicly traded, they co-move with equities, but longer term their ability to pass price increases onto their tenants ties their value to their expected cash flows.

Global Bonds: A small position, as we generally expect the yields on developed country sovereign debt to rise, we nonetheless like exposure to a non-USD denominated safe-haven security in the event that the worst-case scenario is realized, the world economy tanks, and the dollar sells off as it did around Liberation Day on the loss of Fed independence.

Emerging Market Currency/Local Currency Emerging Market Debt/Emerging Market Equities: A small position, as the USD should stay strong while the price of oil is high and interest rates stay where they are currently parked. Emerging Market currencies, however, are rising secularly against their developed market peers, so some exposure here is warranted. Again, these countries’ balance sheets have been improving relative to their developed world peers, and AI technologies should enable rapid human capital development in these countries, allowing them to make up ground against their developed peers quickly and inexpensively. During periods of contracting global growth, EM equities on the whole underperform. This commodity shock, though, will impact commodity exporters and low value-added manufacturers differentially, so it is possible that there is a bit of a net wash.

Global Infrastructure: Effectively the same thesis as with Global REITS, except people don’t live and work inside of this installed capital, and it comes with sovereign risk. Corporate Credit is a bond with equity downside; Infrastructure is an equity with bond downside. We don’t own Corporate Credit1.

Timberland: Demand from housing construction and paper goods is at a low now, as mortgage rates and average home prices make homes unaffordable for the median buyer and thus unattractive for builders to build. Prices reflect this lull in demand. Timberland, however, is a fairly unique commodity in that it has no storage cost: if one can’t sell down stock in the present, one can just store it ‘on the stump’, where instead of degrading or idling, it makes more of itself. Therefore, it is a great investment both as an inflation hedge as well as a store of value: it pays a carry. Further, given the carbon-intensity of building with concrete, and the efficacy of timber as a substitute in commercial building, greater demand for the humble tree can be seen just over the horizon. But don’t take our word for it; just ask the Swedes.

The Fear of God Is the Beginning of Wisdom

We had meant to finish this piece with a few words on where we are in the cycle, recent economic indicators, etc., but that would be to further abuse your already admirable perseverance, dear reader. Suffice it to say that we are bullish the above, and bearish what isn’t. The economy was beginning to tip into slowdown, and Mr. Trump’s incursion-excursion has likely accelerated it. We do not have data yet to confirm this, but the data we do have point in this direction. Ever mindful of the limits of human knowledge, we await with everyone else to see where events might take us.

Global Market Views

Unless it’s on sale!